Budget Information

The Lower Niobrara Natural Resources District (LNNRD) holds an annual budget and levy hearing to allow all constituents the opportunity to ask questions or voice concerns about the current fiscal year’s budget prior to its submission on or before September 30.

The LNNRD is classified as a political subdivision with a fiscal year running from July 1 through June 30. Under current state legislation, all Natural Resources Districts (NRDs) are subject to specific budget and levy limitations. The State of Nebraska limits NRDs to a maximum levy of 4.5 cents per $100.00 of valuation, with an additional 1.0 cent per $100.00 allowed for groundwater management activities, for a total possible levy of 5.5 cents per $100.00 of valuation.

The Nebraska Budget Act requires that all public funds, including non-tax revenues, be reported to the Nebraska Auditor of Public Accounts. In addition to property taxes, the LNNRD receives funding through state and federal grants, resale materials, educational programming, and permitting fees. Each year, an external audit is completed and submitted to the State Auditor in full compliance with state legislation.

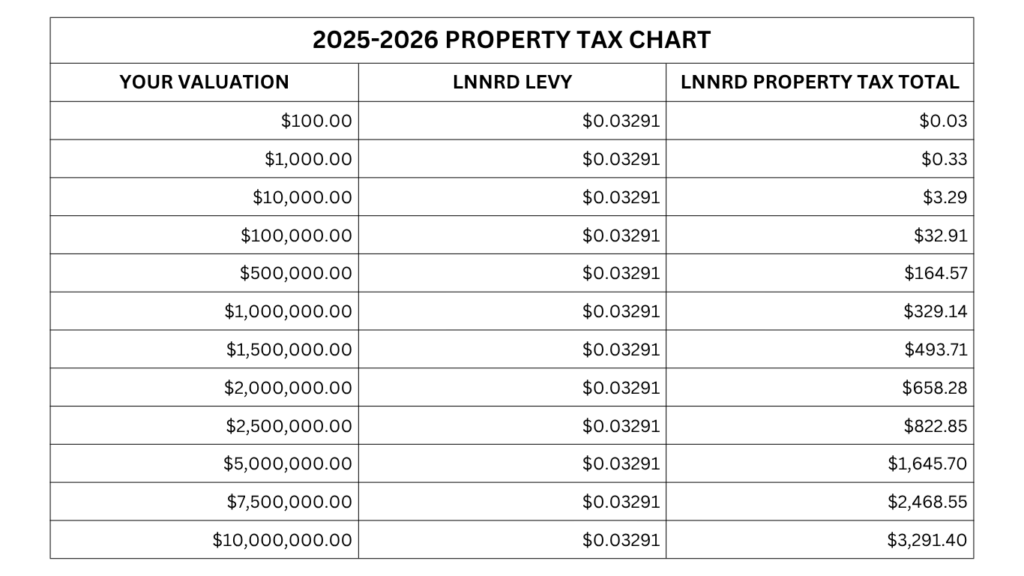

The current LNNRD levy is set at 3.29 cents per $100.00 of assessed valuation.

To estimate the portion of your property tax paid to the LNNRD, multiply your property’s assessed value (divided by 100) by 0.0329.

For example:

- A property valued at $100,000 would contribute approximately $32.90 annually to the LNNRD.

LNNRD 2025-2026 Budget Hearing Notice

Nebraska State Auditor Basic Budget Data Query

Provides a multi-year search of the top 10 most commonly asked about fields on budget forms: Property Tax Request, Outstanding Bonded Indebtedness, Total Disbursements, Total Available Resources, Valuation, and Unused Budget Authority. Also includes links to PDF files of budget forms, if available

Additional Budget information:

The Value of Property: The Basics of Nebraska Property Tax 2025 Edition

Agricultural and Horticultural Land

Nebraska’s agricultural and horticultural land receives a special valuation, allowing it to be taxed based on its current agricultural use rather than potential market value.

This special valuation was first authorized by a 1972 constitutional amendment, with later amendments in 1984 and 1990 creating a separate property class and removing it from the general uniformity clause.

Since 2006, agricultural and horticultural land has been assessed at 75% of its actual value, compared to 100% for residential, commercial, and village property.

To qualify for special valuation, land must:

- Be used primarily for agricultural or horticultural purposes.

- Be located outside the boundaries of any city, village, or sanitary and improvement district (SID).

Land is further divided into subclasses — such as irrigated cropland, dryland, grassland, orchards, nurseries, feedlots, and wasteland — for more accurate comparison and assessment.

Property Tax Levies

Once assessment and equalization are complete, each political subdivision is authorized to determine its tax levy. The uniformity clause of the Nebraska Constitution also applies to the rate of tax imposed, requiring that all taxes within a political subdivision be uniformly applied.

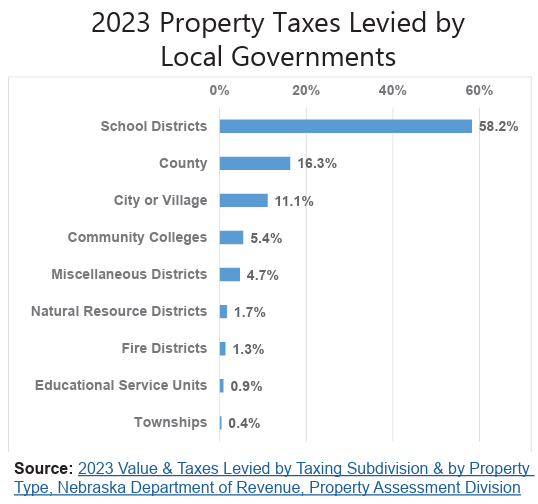

Nebraska has more than 30 types of political subdivisions created by statute, many of which have the authority to levy property taxes. School districts account for the largest portion of most property tax bills, collecting nearly 60% of all property taxes statewide.

Levy Limits by Political Subdivision

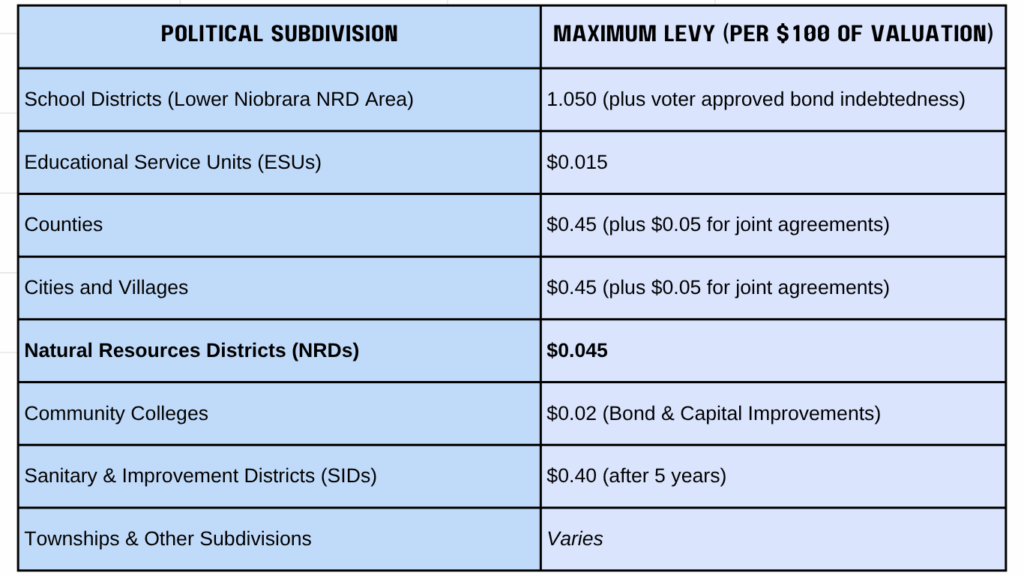

State statutes establish maximum levy limits for most political subdivisions:

- School Districts: May levy up to $1.05 per $100 of valuation, the highest limit among local governments. School districts may also levy separate bond funds approved by voters to repay bonded indebtedness for facility construction or improvement projects

- Educational Service Units (ESUs): Authorized to levy up to $0.015 per $100 of valuation for regional educational services.

- Counties: Constitutionally limited to $0.50 per $100 of valuation. State law restricts counties to $0.45, with an additional $0.05 allowed for joint agreements. Counties may delegate up to $0.15 of the total levy to other entities within the county.

- Cities and Villages: May levy up to $0.45 per $100 of valuation, plus an additional $0.05 for joint agreements. A portion of the levy may be delegated to other entities within the city or village.

- Natural Resources Districts (NRDs): Authorized to levy up to $0.045 per $100 of valuation, with authority for additional levies to carry out programs under the Nebraska Ground Water Management and Protection Act.

Other Taxing Entities

Many other political subdivisions in Nebraska are also authorized to levy property taxes, often within the levy limits of their county or municipality. These include:

County agricultural societies · County fair boards · Joint airport authorities · Airport authorities · Bridge commissions · Cemetery districts · Community redevelopment authorities · Drainage districts · Historical societies · Hospital districts · Irrigation districts · Public building commissions · Railroad transportation safety districts · Reclamation districts · Road districts · Rural water districts · Off-street parking districts · Transit authorities

Most of these entities have specific statutory levy limits and, in some cases, may request voter approval to exceed their levy limit or issue bonds for designated purposes.

Summary

These levy limits help ensure fairness, transparency, and consistency in how property taxes are applied across Nebraska. Each political subdivision must operate within its statutory authority, maintaining balanced and responsible local funding for essential public services.

If you have any question please reach out the LNNRD at LNNRD@LNNRD.ORG or 402-775-2343